You have invested your money in an asset – such as stock, mutual funds, bonds, etc. – and you’re probably thinking, This is awesome! I’m going to make a huge profit! However, the end of the year rolls around and you receive an Informational Tax Reporting Statement from your brokerage agency or mutual fund manager (such as Fidelity or other financial institution) containing a bunch of numbers and information regarding the transactions taken during the year, the income generated by your portfolio, dividends paid, capital gains incurred, and interest income received along with information regarding some expenses. Now, you may be thinking, How do I figure out how much U.S. federal income tax I owe? I don’t understand any of this! If this is you, and you’re reading this post, you’ve come to the right starting place.

What are Dividends vs. Capital Gains?

Dividend income is generally generated when a corporation distributes a portion or all of its profits to its shareholders during the year on a pro rata basis according to each shareholder’s ownership percentage in the Company, whether shares are owned directly or through a fund. Dividends are typically treated as ordinary income and are subject to the tax rate applicable to the shareholder who receives the dividend income.

Certain dividends, called “qualified dividends,” are subject to the preferential long-term capital gains rates. For the dividend to be a “qualified dividend,” the taxpayer, whether directly or indirectly through the fund, must hold the shares for more than 60 days during the 121-day period that begins before the ex-dividend date (which is the date after the dividend has been paid and processed).

Capital gain is generally generated when a taxpayer sells (directly or through a fund) a capital asset, such as stocks, bonds, real estate, or other investment property. Certain capital gains are typically taxed at a rate of 20% if the assets in question have been held by the taxpayer for more than 12 months. If the investment has been held for less than 12 months, the capital gains are classified as short-term and are subject to the higher ordinary individual income tax rates.

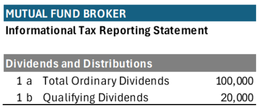

This is best illustrated with an example. Let’s say you received the following Informational Tax Reporting Statement from your fund.

The amount reported as “Qualifying Dividends” is also included in the “Total Ordinary Dividends.” However, the amount included in “Qualifying Dividends” is subject to the lower preferential long-term capital gains rates as opposed to ordinary income, subject to the higher individual tax rates. As such, you would report $80,000 in ordinary income and $20,000 in capital gain.

Understanding Dividends

It’s important to understand which types of dividends are subject to the higher individual tax rates versus those eligible for the lower long-term capital gains rates to properly determine your tax liability for the year in question.

Additionally, if you sell a capital asset, such as real property or other assets held for investment purposes, it’s vital to understand the holding period tax implications related to the sale. If the investor holds the asset for 12 months or less, any resulting capital gain will be considered a short-term capital gain subject to the ordinary individual income tax rates.

Finally, if you are serving as a trustee of a trust, the same rules apply regarding dividends and capital gains. However, trusts are subject to additional regulations governing the distribution of dividends and interest, which must be carefully considered when managing the trust’s tax obligations.

In summary, the above example highlights the importance of consulting with a qualified tax advisor to assist you with reviewing and interpreting the tax forms related to your investments. Doing so ensures accurate reporting and helps prevent overpayment of taxes.

For more information or to seek counsel from our Taxation group, please reach out to request a consultation or call us at 216-696-1422.

_____

Please note that Christine Townsend is licensed only in Massachusetts. This information is provided for general informational purposes only and should not be construed as legal advice. Readers should consult with qualified legal counsel regarding their specific circumstances before taking any action based on the information presented.